First Advantage (FA)

Thesis

Investors have historically treated the background-screening space with hesitancy due to the industry’s macro sensitivity, commodity-like product offerings, and lack of clear differentiation among its constituent companies.

However, First Advantage’s (FA) February announcement of its cash and stock deal to acquire employment background-screening rival Sterling Check (STER) does much to address both the economic cyclicality and competition concerns. The combined FA/STER greatly benefits from FA’s best-in-class management and unprecedented scale- affording more predictable growth, pricing power, cost synergies, higher margins, and ultimately better cash generation.

The pro-forma company trades at less than 11x 2024 EBITDA- a low valuation considering secular tailwinds, a much more achievable high-single digit (HSD) organic annual growth rate over the cycle, and an opportunity for 500 basis points+ (bps) of margin expansion.

Assuming the low end of both companies’ pre-merger target growth algorithms along with conservative margin improvement, in 2026, FA would produce nearly $600M in EBITDA, $300M in FCF (9x), and deleverage a full two turns to just over 2x net. Holding the 10.5x EBITDA multiple constant results in 25% three-year IRR.

In a downside case, assuming no synergies are realized and the multiple compresses to a punitive 9x, still suggests a $19 stock and HSD IRR.

Background

First Advantage and other full-service screeners (or “consumer reporting agencies”, CRA) offer employers services including criminal background checks, drug screens, work verification, industry-specific licensure compliance verification, and a host of other related products. As most revenue is derived from pre-onboarding activities (i.e., the background checks), FA and its peers’ performance has roughly tracked the rate of worker churn and hiring trends (quantity) in their customers’ respective industries. The most frequently cited hiring data are the monthly Job Openings and Labor Turnover Survey reports (JOLTS). However, the quality of the reports have been called into question and the specific outputs offer little predictive insight to the CRA’s performance.

The screening space remains fragmented with the “big three”- First Advantage, Sterling, and HireRight (HRT)- collectively accounting for 25% to 35% of the U.S. market (and a far smaller percentage internationally), with the balance comprised of a long-tail of tech-forward challengers (e.g, Checkr) and legacy mid-market point solutions. FA, STER, and HRT have pulled away from the SMB segment and now focus almost exclusively on enterprise clients (defined by FA as those that contribute $500,000 or more in annual revenues) with high hiring volumes, extensive system integration requirements, and often more complex (higher ticket) screens.

After several years of largely acquisition-led growth under private equity ownership, in late 2021, the Big Three went public- capitalizing on the “Great Resignation’s” strong demand trends and the period’s heady IPO market. Since then, due to a combination of hiring slowdown, market pullback, and investor skepticism about the quality and predictability of the checker business, the Three have traded poorly- despite their sponsors retaining sizable stakes. Rather than continue to flounder in the public eye, in early February, HRT agreed to be retaken private. Leaving FA/STER as the sole listed background checking company.

FA’s Acquisition of STER

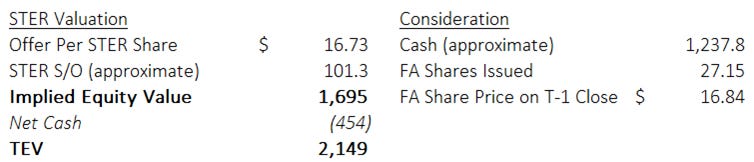

Concurrent with its Q4 earnings, FA announced the acquisition of STER for 27.15M shares and approximately $1.2B - financed with $1.8B in additional debt. The transaction is expected to bring $50M in annual run rate synergies within 18-24 months of the targeted Q3 closing date. FA’s CEO, Scott Staples, will lead the combined company.

Why Now?

The merger materially strengthens FA’s business and attractiveness as an investment:

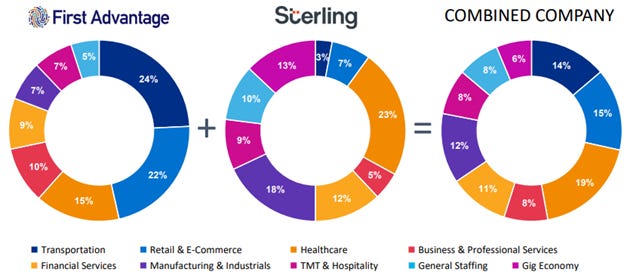

Reduced Cyclicality: FA has outsized exposure to the recession-sensitive transportation and retail industries. The combination with STER adds more stable healthcare customers (COVID period aside) and, most importantly, smooths FA’s aggregate cyclicality by spreading exposure across industry verticals- each of which often have different cyclical (and seasonal) timing in their peak/trough hiring demands. The addition of STER’s clients also dilutes FA’s individual customer concentration risk (12% of 2023 sales were to a single customer- rumored to be FedEx).

While the background checkers’ fortunes will always fluctuate based on the broader macro, customer industry diversification lowers idiosyncratic risk and creates more predictable and forecastable growth in topline and earnings. Ultimately allowing for tighter cash management and better capital allocation.

All About Data

Data Moat: Pooling together the two companies’ decades of accumulated background check results creates an unparalleled data lake. More data means a greater percentage of checks can be completed with information already on hand- reducing FA’s dependency and expenditure on third party data vendors. This lowers turnaround times and the cost per check- offering FA a differentiated service and pricing (and/or margin) advantage against smaller competitors. A larger data repository, coupled with FA and STER’s extensive investments in automation, puts the company at a distinct advantage versus subscale peers.

Collecting Data: When FA does need to turn to external vendors, its larger scale (20%+ share of the U.S. background check industry) undoubtedly gives the company a stronger negotiating position as it can credibly promise suppliers higher volume and more consistent orders.

The combined firm’s size expands opportunities to vertically integrate by bringing larger portions of the third-party sourcing in-house. Either via outright acquisition (as both companies have frequently done) or by building the requisite data retrieval infrastructure internally.

As an example of how scale benefits the latter, criminal checks often require accessing county-level court records. An estimated one third of the approximately 3,150 counties in the U.S. do not have electronic court systems. The CRA must send a runner to physically show up at the courthouse (and hope the right clerk is there) to obtain the records- a highly manual, inefficient, and expensive process that necessitates contracting a local runner. However, if the checker were to have sufficient demand in a given jurisdiction, then it may make economic sense to incur the upfront/fixed costs of hiring full time runners or even offering to digitize the court’s records (to be used internally and perhaps sold to other CRAs) as the costs can be (profitably) amortized across the higher volume.

One Less Competitor: With the “Big Three” transitioning to “First Advantage” and “HireRight, that number two at half the size,” competitive pressures will likely ease- particularly in the core enterprise customer space.

Lower Sales & Marketing Intensity: With less competition, there is room for margin expansion as sales and marketing spend is dialed back. Both client retention and new business win costs may even fall as FA becomes the “default” CRA for enterprise. However, the considerable switching costs characteristic of the tightly integrated enterprise cohort probably negate any meaningful churn or unexpected wins in the near term.

Pricing: While the Big Three have generally avoided competing on price, there are rumors STER has been discounting to capture market share (partially explaining STER’s EBITDA margins running 400 to 500 basis points below target). To the extent this is material, expect pricing discipline and margin improvement to return upon the deal closing.

FA CEO Scott Staples at JPM Conference, November 2023: “We don't like to talk about pricing a lot. Our clients get to read and hear everything that we say. So, we're very careful about (public pricing discussion). We do have the right in every one of our contracts to pass on CPI increases every year and have done that selectively in each of the past 3 years. We have raised some package costs and passed on some fees as well over the last several years. (All done) selectively.”

Key Performance Indicators (KPIs): To date, the background checkers have disclosed frustratingly little in the way of KPIs, such as average revenue per user, churn, exact retention rates, number and type of checks performed, etc. With HRT soon going private, FA remains the only public CRA and the sole remaining option for investors who want to be involved in the space. Without close peers directly competing for investor dollars, this is an excellent opportunity for management to release detailed KPIs- providing investors with transparency beyond simple financials. Allowing for a view into the actual business’ underlying performance and more informed confidence in company’s near-term trajectory.

FA’s Operational Knowledge & Conservative Cost Synergies

Operational Spend: Since 2019, FA has managed to grow revenue at a faster annual rate, to a higher absolute dollar value, with operating expenses as a percentage of sales nearly 1000 bps lower than STER’s. Even more impressively, FA achieved this growth by spending fewer total sales, general, and administrative (SG&A) dollars than STER.

Expect FA’s continuing CEO, Scott Staples, and senior management team to apply their operational chops to help close the gaping 500 bps EBITDA margin gap.

Merger Synergies: The company believes it can capture $50M of run-rate synergies in the 18 to 24 months post-close. Management has stressed these are entirely “low hanging fruit” cost synergies: sharing of databases that lower reliance on and fees paid to third parties, consolidation of tax, audit, insurance, and public company functions, etc.

Often bandied, but seldom realized, revenue and cross-sell synergies are “upside” not included in the $50M.

Valuation

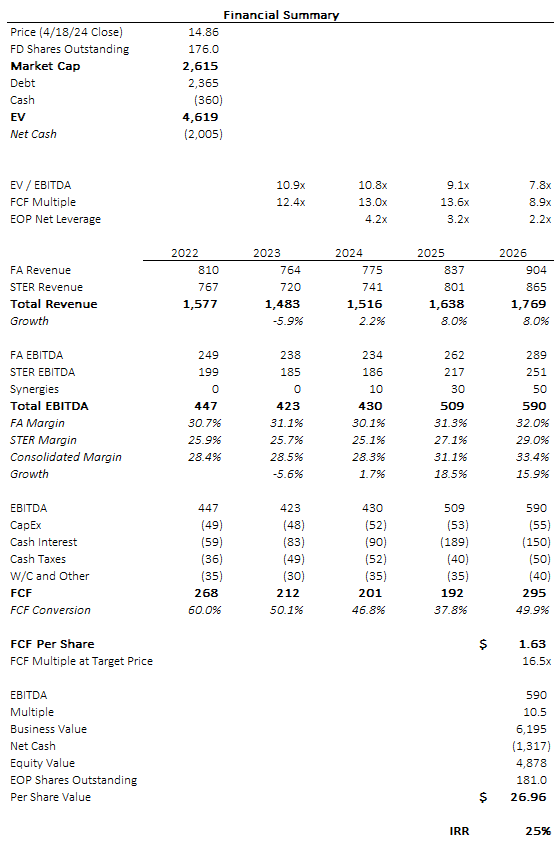

Revenue Growth: Both FA and STER have consistently targeted HSD organic growth, with 2% to 4% of that as macro-driven “base growth.” While long term data is limited and the COVID period labor market whiplash makes the past few years difficult to analyze, the two companies achieved 8%+ growth prior from 2018 to 2019 (with minimal M&A). When paired with HSD five-year CAGRs ending 2023 (acknowledging some inorganic contribution), it seems fair to assume a normalized 8% rate beginning in 2025, with north of $1.75B in 2026 sales.

Any outsized improvement in the macro and/or revenue synergies (e.g., if the added scale leads to more successful cross-selling, additional new wins, better retention, etc.) could push revenue growth into LDDs.

EBITDA Margins: Synergies, efficiencies, and pricing push margins beyond FA’s 30% to the lower-mid 30%’s, for $590M of EBITDA in 2026. Note that gross margins also benefit from added background check volume:

CEO of Accurate Background (4th largest CRA): “With a $1.5 billion revenue company, you probably could get to 35-plus margins because you don't need more SG&A. Gross margins will improve slightly because you're getting efficient. With less SG&A, (much of the added revenue) is just going to drop the bottom line.

The problem with the gross margins is the amount of people who actually have records. Most don't have records. The ones who are clear (without records) fly right through the system- those are the most profitable searches. (But) people (with records require) more customer service (and) cost the most. But with scale, (the checker captures) more and more people who are clear and run through the system (at lower cost per check).”

Free Cash Flow and Leverage: By deleveraging from 4x net at deal close to 2x by 2026, interest expense declines, and conversion from EBITDA returns to the 50% range for nearly $300M in 2026 FCF. Once in the company’s stated 2x to 3x target range, FA can resume buybacks or further tuck-in M&A.

Applying the current multiple of 10.5x on $590M of 2026 EBITDA nets a $27.00 share price, for a 25% three-year IRR- all with a 2x turns leverage reduction in leverage.

Bottom Line: the checkers will always be macro-dependent, quasi-black box businesses. But FA’s acquired scale, post-COVID normalization of the labor market, strong and improving economics, and significant runway for both topline growth and per-share value creation make for a compelling long.

Risks

Though the combined company will be more resilient, background checkers are inextricably linked to the business cycle. Growth will inevitably be lumpy, and one must believe management will adjust costs and capital allocation accordingly. At over 4x net levered, FA carries a high debt/interest burden and will be particularly sensitive to quarterly results, with limited cash deployment opportunities outside of paydown (i.e., buybacks) for the next few years. Debt servicing needs might also prevent necessary investments or tactical M&A to defend against the countless CRA tech-forward start-ups.

With the current anti-trust environment, and optics of the number one merging with the number two, there is a chance the deal is blocked or requires onerous concessions that remove the considerable upside.

Finally, there may be some enduring investor stigma. The background checkers IPOed into a hot capital and labor market, having since traded poorly as both cooled. Because of the absence of disclosed KPIs, there is little accessible fundamental data that might indicate improvement in the underlying business. This leaves disappointing (negative growth) recent past financial performance as the only readily observable metric. Until there is evidence of a positive inflection, for many investors, FA will remain a “show me” story.

Thoughts on FA now?